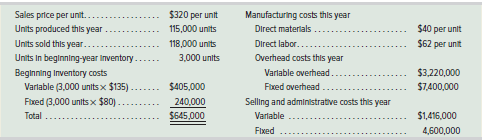

Oak Mart, a producer of solid oak tables, reports the following data from its second year of business.

The Correct Answer and Explanation is :

To prepare the income statements for Oak Mart using both variable and absorption costing methods, we need specific financial data, such as sales revenue, variable costs, fixed costs, and production volumes. Since this information isn’t provided, I can explain the general approach to preparing these income statements and the key differences between the two costing methods.

1. Variable Costing Income Statement:

Under variable costing, only variable manufacturing costs are included in the cost of goods sold (COGS). Fixed manufacturing overhead is treated as a period expense and is deducted in full in the period incurred.

Format:

- Sales Revenue

- Less: Variable Costs

- Variable Cost of Goods Sold

- Variable Selling and Administrative Expenses

- Contribution Margin (Sales Revenue minus Total Variable Costs)

- Less: Fixed Costs

- Fixed Manufacturing Overhead

- Fixed Selling and Administrative Expenses

- Net Operating Income (Contribution Margin minus Total Fixed Costs)

Example:

If Oak Mart’s sales revenue is $500,000, variable COGS is $200,000, variable selling and administrative expenses are $50,000, fixed manufacturing overhead is $100,000, and fixed selling and administrative expenses are $30,000, the income statement would be:

- Sales Revenue: $500,000

- Less: Variable Costs:

- Variable COGS: $200,000

- Variable Selling and Administrative Expenses: $50,000

- Contribution Margin: $250,000

- Less: Fixed Costs:

- Fixed Manufacturing Overhead: $100,000

- Fixed Selling and Administrative Expenses: $30,000

- Net Operating Income: $120,000

2. Absorption Costing Income Statement:

Absorption costing allocates all manufacturing costs, both variable and fixed, to the cost of goods sold. Fixed manufacturing overhead is included in the inventory valuation and expensed as part of COGS when the inventory is sold.

Format:

- Sales Revenue

- Less: Cost of Goods Sold

- Direct Materials

- Direct Labor

- Variable Manufacturing Overhead

- Fixed Manufacturing Overhead (allocated to units sold)

- Gross Profit (Sales Revenue minus COGS)

- Less: Selling and Administrative Expenses

- Variable Selling and Administrative Expenses

- Fixed Selling and Administrative Expenses

- Net Operating Income (Gross Profit minus Total Selling and Administrative Expenses)

Example:

Using the same figures as above, the absorption costing income statement would be:

- Sales Revenue: $500,000

- Less: Cost of Goods Sold:

- Direct Materials: $100,000

- Direct Labor: $50,000

- Variable Manufacturing Overhead: $30,000

- Fixed Manufacturing Overhead (allocated to units sold): $100,000

- Gross Profit: $220,000

- Less: Selling and Administrative Expenses:

- Variable Selling and Administrative Expenses: $50,000

- Fixed Selling and Administrative Expenses: $30,000

- Net Operating Income: $140,000

3. Explanation of Differences:

The primary difference between the two income statements lies in the treatment of fixed manufacturing overhead:

- Variable Costing: Fixed manufacturing overhead is treated as a period expense and is deducted in full in the period incurred. This method provides a clearer picture of the contribution margin and is useful for internal decision-making, as it shows how much revenue is available to cover fixed costs and contribute to profit.

- Absorption Costing: Fixed manufacturing overhead is allocated to each unit produced and included in the inventory valuation. This means that some fixed costs are deferred in inventory and expensed as part of COGS when the inventory is sold. This method is required for external financial reporting under Generally Accepted Accounting Principles (GAAP) and provides a more comprehensive view of product costs.

The choice between these costing methods can significantly impact reported profitability, especially when production and sales volumes differ. Under absorption costing, if production exceeds sales, some fixed manufacturing overhead costs are deferred in inventory, leading to higher reported profits. Conversely, under variable costing, fixed manufacturing overhead is expensed in the period incurred, so profits are not affected by changes in inventory levels.

Understanding these differences is crucial for management when making pricing, production, and inventory decisions, as well as for external stakeholders analyzing the company’s financial health.