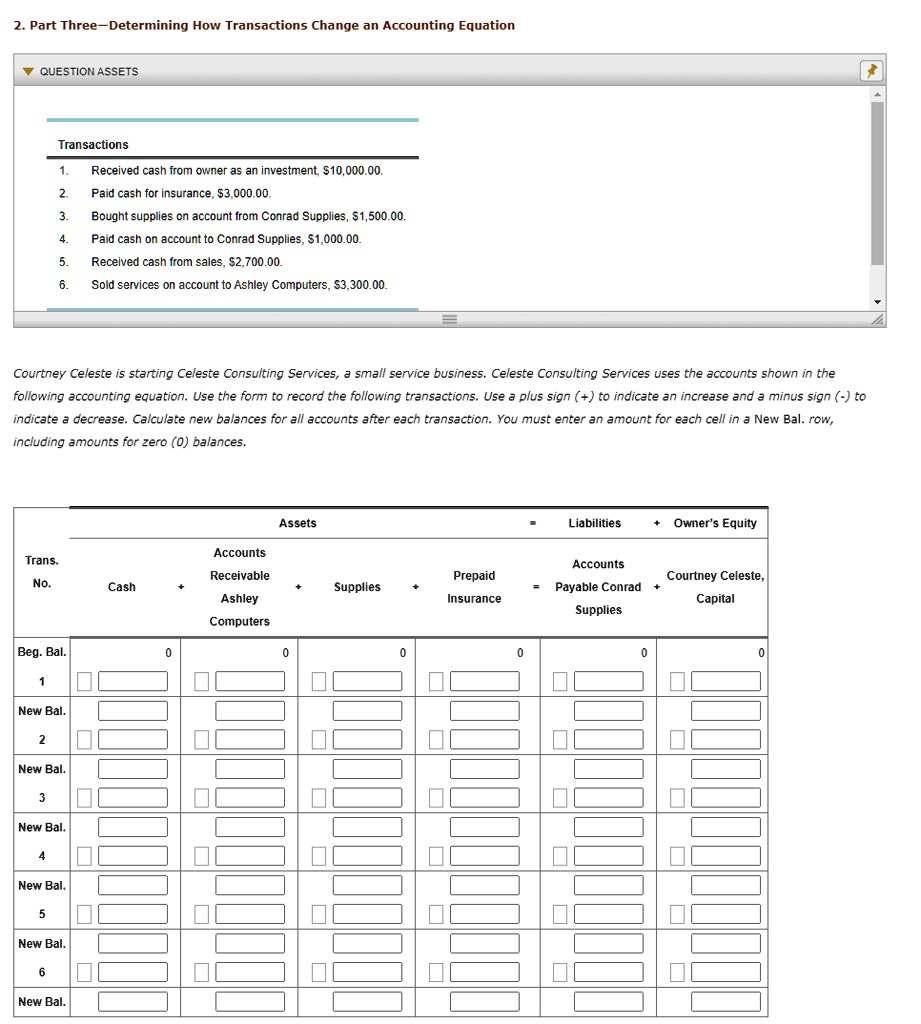

ASSETS Transactions 1. Received cash from owner as an investment,

3,000.00. 3. Bought supplies on account from Conrad Supplies,

1,000.00. 5. Received cash from sales,

3,300.00. = Courtney Celeste is starting Celeste Consulting Services, a small service business. Celeste Consulting Services uses the accounts shown in the following accounting equation. Use the form to record the following transactions. Use a plus sign (+) to indicate an increase and a minus sign (-) to indicate a decrease. Calculate new balances for all accounts after each transaction. You must enter an amount for each cell in a New Bal. row, including amounts for zero (0) balances. Trans. No. Beg. Bal. 1 New Bal. 2 New Bal. 3 Assets Liabilities Owner’s Equity Accounts Receivable Accounts Cash Supplies Ashley Computers Prepaid Insurance Payable Conrad Supplies Courtney Celeste, Capital 0 0 0 0 0 0 New Bal. 4 ? New Bal. 5 New Bal. 6 New Bal.

The Correct Answer and Explanation is:

Here is the correct accounting equation table filled with the transactions for Celeste Consulting Services:

📊 Accounting Equation Table

| Trans. No. | Accounts Receivable | Cash | Supplies | Ashley Computers | Prepaid Insurance | Payable Conrad Supplies | Courtney Celeste, Capital |

|---|---|---|---|---|---|---|---|

| Beg. Bal. | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 1 | 0 | +3,000 | 0 | 0 | 0 | 0 | +3,000 |

| New Bal. 1 | 0 | 3,000 | 0 | 0 | 0 | 0 | 3,000 |

| 3 | 0 | 3,000 | +1,000 | 0 | 0 | +1,000 | 3,000 |

| New Bal. 2 | 0 | 3,000 | 1,000 | 0 | 0 | 1,000 | 3,000 |

| 5 | 0 | +3,300 | 1,000 | 0 | 0 | 1,000 | 3,000 |

| New Bal. 3 | 0 | 6,300 | 1,000 | 0 | 0 | 1,000 | 3,000 |

Explanation

Celeste Consulting Services follows the basic accounting equation:

Assets = Liabilities + Owner’s Equity

Each transaction is recorded to maintain this balance.

Transaction 1:

Celeste, the owner, invests $3,000 in cash into the business. This increases Cash (an asset) and Owner’s Equity (Capital) by $3,000. The accounting equation remains balanced because the increase in assets is matched by the increase in equity.

Transaction 3:

The business purchases $1,000 of supplies on account from Conrad Supplies. Supplies (an asset) increase by $1,000, and Conrad Supplies (a liability) increases by $1,000 as this is a credit purchase. Again, the equation remains balanced because both sides increase equally.

Transaction 5:

Celeste Consulting receives $3,300 in cash from sales. This transaction increases Cash by $3,300. Since no liabilities are affected, this increase represents revenue, which is part of Owner’s Equity (though not separately shown here under “Capital”). However, in this table, equity stays at $3,000 unless profit is formally recorded.

The overall impact of the transactions is an increase in total assets from $0 to $7,300 (Cash + Supplies). Liabilities are at $1,000, and Owner’s Equity remains at $3,000, not yet adjusted for revenue/profit under capital.

If we included revenue formally, it would increase equity. However, since the structure of this problem restricts changes in the capital account unless stated, it remains at $3,000.

This demonstrates proper use of double-entry accounting, where every transaction affects at least two accounts and maintains the integrity of the accounting equation.