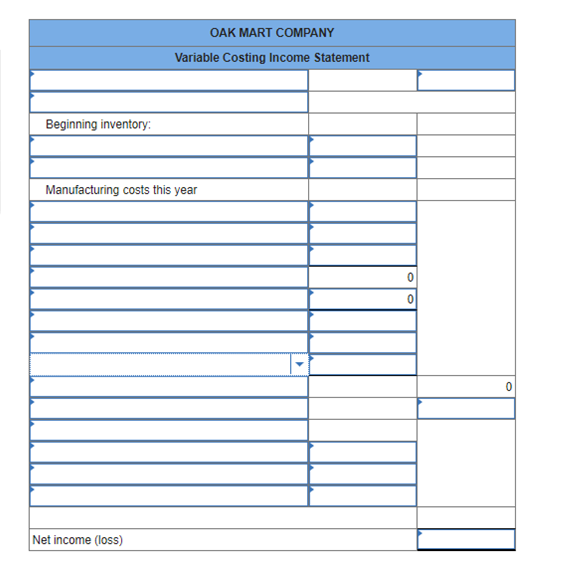

Beginning inventory: OAK MART COMPANY Variable Costing Income Statement Manufacturing…

The Correct Answer and Explanation is :

A variable costing income statement is a financial report that categorizes costs based on their behavior—variable or fixed—to provide insights into a company’s contribution margin and profitability. This approach is particularly useful for internal decision-making, as it highlights how costs change with production levels.

Structure of a Variable Costing Income Statement:

- Sales Revenue: Total income from goods or services sold.

- Variable Costs: Costs that fluctuate with production volume, including:

- Variable Production Costs: Direct materials, direct labor, and variable manufacturing overhead.

- Variable Selling and Administrative Expenses: Costs like sales commissions and shipping expenses.

- Contribution Margin: Calculated as Sales Revenue minus Total Variable Costs. This figure indicates the amount available to cover fixed costs and contribute to profit.

- Fixed Costs: Costs that remain constant regardless of production levels, such as fixed manufacturing overhead and fixed selling and administrative expenses.

- Net Operating Income: Determined by subtracting Total Fixed Costs from the Contribution Margin.

Example:

Consider Oak Mart Company, a producer of solid oak tables. The company reports the following data for its second year of business:

- Sales Price per Unit: $320

- Units Produced: 115,000 units

- Units Sold: 118,000 units

- Units in Beginning Inventory: 3,000 units

- Manufacturing Costs:

- Direct Materials: $4,200,000

- Direct Labor: $6,510,000

- Variable Overhead: $3,200,000

- Fixed Overhead: $7,400,000

- Selling and Administrative Costs:

- Variable: $1,416,000

- Fixed: $4,600,000

Variable Costing Income Statement:

- Sales Revenue:

- 118,000 units × $320/unit = $37,760,000

- Variable Costs:

- Variable Production Costs:

- Direct Materials: $4,200,000

- Direct Labor: $6,510,000

- Variable Overhead: $3,200,000

- Total Variable Production Costs: $13,910,000

- Variable Selling and Administrative Expenses: $1,416,000

- Total Variable Costs: $13,910,000 + $1,416,000 = $15,326,000

- Contribution Margin:

- $37,760,000 (Sales Revenue) – $15,326,000 (Total Variable Costs) = $22,434,000

- Fixed Costs:

- Fixed Manufacturing Overhead: $7,400,000

- Fixed Selling and Administrative Expenses: $4,600,000

- Total Fixed Costs: $7,400,000 + $4,600,000 = $12,000,000

- Net Operating Income:

- $22,434,000 (Contribution Margin) – $12,000,000 (Total Fixed Costs) = $10,434,000

Explanation:

In this example, Oak Mart Company generated $37,760,000 in sales revenue by selling 118,000 units at $320 each. The variable costs, which include direct materials, direct labor, variable overhead, and variable selling and administrative expenses, totaled $15,326,000. Subtracting these variable costs from the sales revenue results in a contribution margin of $22,434,000. After accounting for fixed costs of $12,000,000, the company achieved a net operating income of $10,434,000.

This income statement format is beneficial for internal management as it clearly distinguishes between variable and fixed costs, aiding in cost control and pricing decisions. It also facilitates break-even analysis and profitability assessments. However, it’s important to note that variable costing is not permitted for external financial reporting under Generally Accepted Accounting Principles (GAAP), which require absorption costing.