Coney Island Entertainment issues $1.500.000 of 5% bonds, 15 years, with interest payable samiannually on. Ane 30 and December 31 each year Calculate the issue price of a bond and congrets the first three rows of an amortization schedule when 1 Required: The market interest rate is 5% and the bonds issue at face amount EXOL 51. PV of $1. EVA ot, and PVA OD1) (Use appropriate factor(s) from the tables provided. Do not round interest rate factors.) 2. 0.0 points The market interest rate is 6% and the bonds issue at a discount. (EV of $1. PV of $1. EVA of $1. and PVA$1) (Use appropriate factor(s) from the tables provided. Do not round interest rate factors.) Jenny

The Correct Answer and Explanation is :

To calculate the issue price of a bond and to generate an amortization schedule for the first three rows, we need to follow several steps. Let’s break down the problem with the two different interest rates and explain the calculations.

1. Market Interest Rate is 5%:

In this case, the coupon rate (5%) is equal to the market interest rate (5%). This means the bond will be issued at its face value.

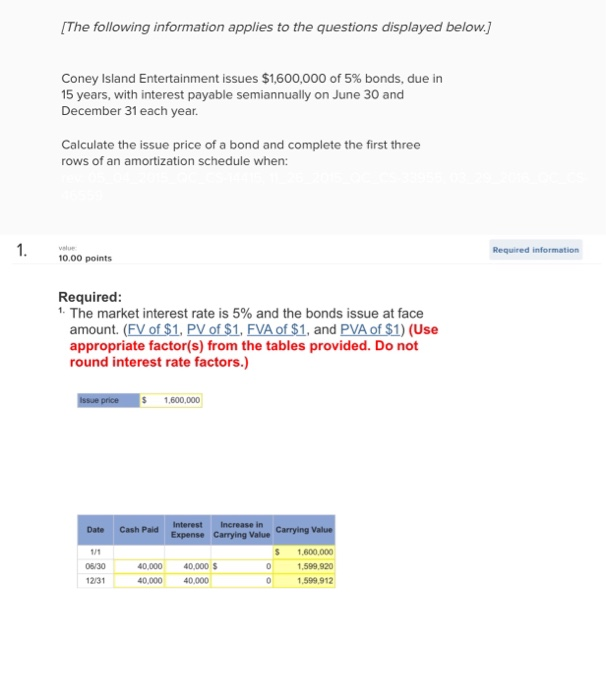

- Face Value of the Bond: $1,500,000

- Coupon Rate: 5% (annually, but interest is paid semi-annually, so the coupon rate is divided by 2, and we use 2.5% per period)

- Number of Periods (n): 15 years × 2 = 30 periods (semi-annual payments)

- Market Rate per Period (i): 5% annually ÷ 2 = 2.5% per period.

The price of the bond is the sum of the present value of the interest payments (annuity) and the present value of the principal (lump sum) at maturity.

Using the present value formula:

- PV of Coupons:

[ \text{PV of Coupons} = C \times PVA(i, n) ]

Where:- ( C = 1,500,000 \times 5\% \div 2 = 37,500 ) (semiannual coupon payment)

- ( PVA(i, n) ) is the present value of an annuity factor for the market rate, at 2.5% for 30 periods.

- PV of Face Value:

[ \text{PV of Face Value} = 1,500,000 \times PV(i, n) ]

Where ( PV(i, n) ) is the present value of a single lump sum factor for the market rate, at 2.5% for 30 periods.

Because the coupon rate and market rate are the same, the bond will be priced at its face value of $1,500,000.

2. Market Interest Rate is 6%:

When the market interest rate is greater than the coupon rate (6% versus 5%), the bond will be issued at a discount. The issue price will be less than the face value.

- Coupon Payment:

[ 1,500,000 \times 5\% \div 2 = 37,500 \text{ (semiannual coupon)} ] - Market Rate per Period (i): 6% annually ÷ 2 = 3% per period.

Now, we calculate the present value of the bond’s cash flows:

- PV of Coupons (Annuity):

[ \text{PV of Coupons} = 37,500 \times PVA(3\%, 30) ] - PV of Face Value (Lump Sum):

[ \text{PV of Face Value} = 1,500,000 \times PV(3\%, 30) ]

The price of the bond will be the sum of these two present values. Since the market rate is higher than the coupon rate, the price will be lower than the face value, reflecting the bond being sold at a discount.

Amortization Schedule

Once we have the bond price, the amortization schedule can be prepared. Here’s how it works:

- The interest expense is calculated by multiplying the bond’s book value at the start of the period by the market interest rate per period.

- The amortization of the discount is the difference between the interest expense and the coupon payment.

- The book value of the bond increases by the amortized discount after each period.

First Three Rows Example:

For the first three rows of the amortization schedule when the market rate is 6%:

| Period | Interest Expense | Coupon Payment | Amortization of Discount | Book Value |

|---|---|---|---|---|

| 1 | (Book Value × 3%) | 37,500 | (Interest – Coupon) | (Previous Book Value + Amortization) |

| 2 | (New Book Value × 3%) | 37,500 | (Interest – Coupon) | (Previous Book Value + Amortization) |

| 3 | (New Book Value × 3%) | 37,500 | (Interest – Coupon) | (Previous Book Value + Amortization) |

For this, the exact values for Interest Expense, Amortization of Discount, and Book Value would require calculating the present value factors from the appropriate tables, which you can do using financial calculators or spreadsheet functions for more accurate results.

Conclusion

- When the market rate equals the coupon rate (5%), the bond is issued at face value.

- When the market rate is greater than the coupon rate (6%), the bond is issued at a discount, and the amortization schedule reflects the gradual increase in book value as the discount is amortized over time.

By following these calculations and using appropriate factors from financial tables, you can calculate the bond’s issue price and create a detailed amortization schedule.