It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest. We address ourselves, not to their humanity but to their self-love, and never talk to them of our own necessities but of their advantages. Do you agree with this quotation from Adam Smith s classic, The Wealth of Nations? How are our dinner and their self-interest related to the price system? What does Smith assume to be the motives of firms and households? 6. In the chapter we used a simple idea of a production possibilities boundary to illustrate the concepts of scarcity, choice, and opportunity cost. We assumed there were only two goods call them X and Y. But we all know that any economy produces many more than just two goods. Explain why the insights illustrated in Figure 1-2 on page 8 are more general, and why the assumption of only two goods is a useful one.

The correct answer and explanation is :

Adam Smith’s famous quotation from The Wealth of Nations reflects a central tenet of economic theory: individuals and firms act in their own self-interest to maximize their utility and profits. Smith argues that while we rely on others—such as the butcher, brewer, or baker—to provide us with the goods we consume, it is not out of their benevolence but out of their pursuit of their own self-interest. In other words, they provide for us because it serves their financial interests to do so, not because they are motivated by a desire to help us. This concept highlights the role of self-interest as a driving force in the economy.

Relation to the Price System:

The price system emerges from the self-interest of individuals and firms. Prices reflect the balance of supply and demand in a market. In this system, producers seek to maximize profits, while consumers seek to maximize satisfaction. When we address the butcher or baker, we appeal to their self-interest—offering them a price that reflects the value they place on their goods or services. This self-interest leads to the creation of prices that allocate resources efficiently in the economy. The price system helps balance production and consumption by providing incentives for producers to supply goods and services and for consumers to demand them.

Motives of Firms and Households:

Smith assumes that firms aim to maximize profits, and households aim to maximize utility or satisfaction. Firms produce goods and services to sell at prices that allow them to earn profits, while households purchase goods and services that maximize their well-being, given their income and the prices they face.

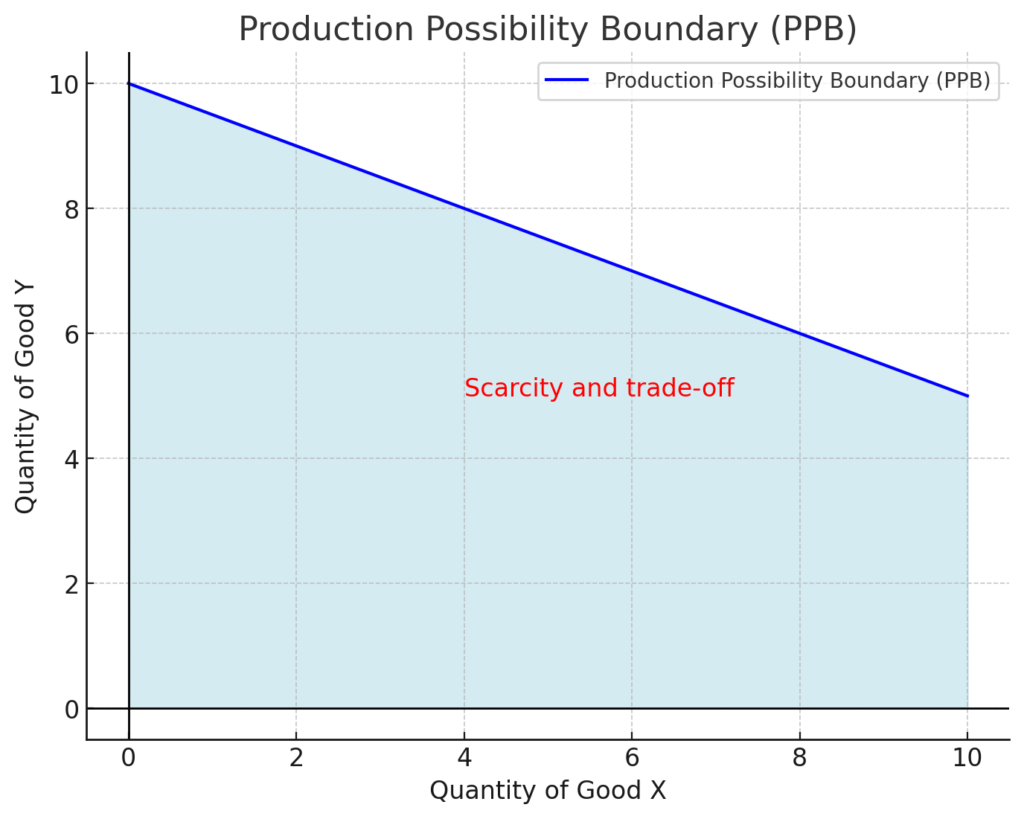

The Two-Good Assumption:

The simple model of the production possibilities boundary (PPB) often assumes only two goods (X and Y) to illustrate the fundamental economic concepts of scarcity, choice, and opportunity cost. This model simplifies the analysis and allows us to visualize trade-offs, such as how producing more of one good (say X) requires sacrificing some of the other good (Y). However, the real world involves many more goods and services, and the economy faces much more complex decisions regarding resource allocation.

The insights from the two-good model, however, are generalizable. The key concepts of scarcity and opportunity cost remain relevant regardless of the number of goods. The PPB still illustrates the need to make choices due to limited resources and the trade-offs involved. The two-good model is a useful simplification because it makes it easier to grasp these economic principles before expanding to more complex scenarios with many goods and services.

Below is an illustration of the Production Possibility Boundary (PPB) using two goods (X and Y). The curve shows the maximum possible output of X and Y that can be produced with the available resources.

The chart above illustrates the concept of the Production Possibility Boundary (PPB) with two goods, X and Y. The curve represents the trade-offs involved in allocating limited resources between the two goods. The area under the curve shows the possible combinations of X and Y that can be produced. The notion of scarcity is reflected in the fact that producing more of one good requires sacrificing some of the other. The PPB is a useful simplification for understanding key economic concepts like scarcity and opportunity cost, even though real-world economies produce more than two goods.