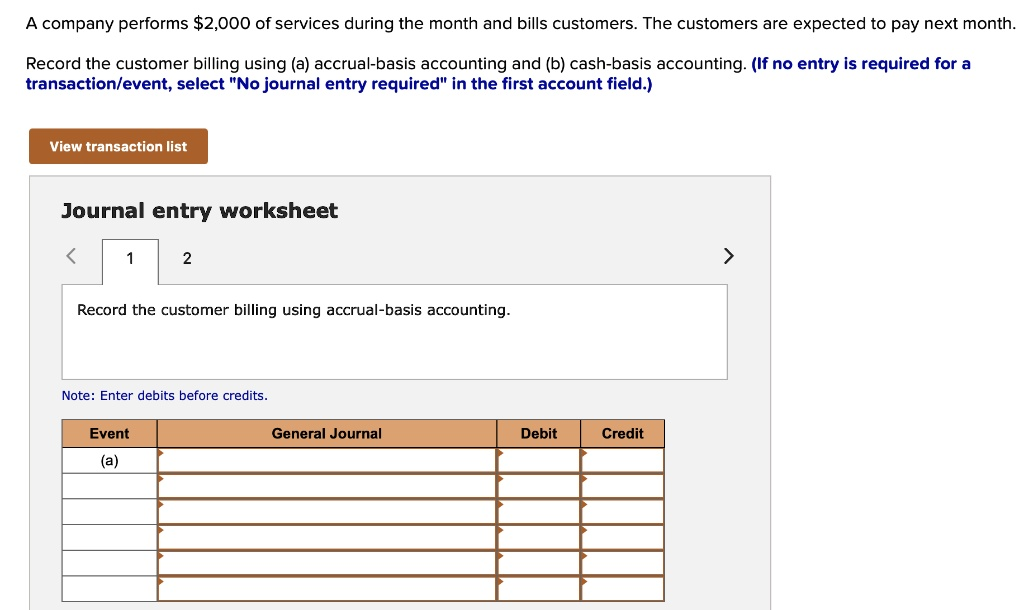

A company performs $2,000 of services during the month and bills customers. The customers are expected to pay next month. Record the customer billing using (a) accrual-basis accounting and (b) cash-basis accounting. (If no entry is required for a transaction/event, select “No journal entry required” in the first account field.) View transaction list Journal entry worksheet < 1 2 Record the customer billing using accrual-basis accounting. Note: Enter debits before credits. Event (a) General Journal Debit Credit >

The Correct Answer and Explanation is:

Completed Journal Entry Worksheet

Page 1: Accrual-Basis Accounting

| Event | General Journal | Debit | Credit |

| (a) | Accounts Receivable | 2,000 | |

| Service Revenue | 2,000 | ||

Page 2: Cash-Basis Accounting

| Event | General Journal | Debit | Credit |

| (b) | No journal entry required | ||

Explanation

This exercise highlights the fundamental difference between accrual-basis and cash-basis accounting, which lies in the timing of revenue recognition.

Part (a): Accrual-Basis Accounting

Under the accrual basis, revenue is recognized when it is earned and realizable, regardless of when cash is received. This is known as the revenue recognition principle. In this scenario, the company performed $2,000 of services during the month, which means it has earned the revenue.

The corresponding journal entry reflects this principle. A debit is made to Accounts Receivable for $2,000. Accounts Receivable is an asset account that represents the money owed to the company by its customers for goods or services already delivered. The debit increases this asset, showing the company has a claim to future cash. A credit is made to Service Revenue for $2,000. Crediting a revenue account increases its balance, reflecting the income the company earned during the period. This method provides a more accurate picture of a company’s financial performance for the month because it matches the revenue to the period in which the work was actually done.

Part (b): Cash-Basis Accounting

Under the cash basis, revenue is recognized only when cash is physically received. The timing of when the service was performed is irrelevant. Since the problem states that customers are expected to pay next month, no cash was collected during the current month for the services performed.

Therefore, for the current period, there is no transaction to record under the cash-basis method. The correct action is to make “No journal entry required.” The transaction would only be recorded in the following month when the company actually receives the $2,000 cash payment from its customers. At that future time, the entry would be a debit to Cash and a credit to Service Revenue