The Correct Answer and Explanation is:

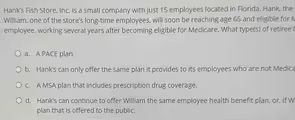

The correct answer is d. Hank’s can continue to offer William the same employee health benefit plan, or, if William prefers, offer a plan that is offered to the public.

Here is an explanation:

The key to this question lies in the Medicare Secondary Payer (MSP) rules and the size of the company. Hank’s Fish Store has only 15 employees, which classifies it as a “small employer” under MSP regulations, as the threshold is 20 employees. The rules for small employers are different from those for larger companies.

For a small employer with fewer than 20 employees, Medicare is the primary payer for active employees who are age 65 or older and are eligible for Medicare. The employer’s group health plan, if the employee chooses to remain on it, becomes the secondary payer. This means Medicare pays for medical claims first, and the company’s health plan pays second for any remaining costs it covers.

Because of this, a small employer has more flexibility. They are not required to offer the same plan to Medicare-eligible employees as they do to other employees. Let’s look at why option (d) is the best choice:

- “Hank’s can continue to offer William the same employee health benefit plan”: This is a valid option. Hank’s can allow William to stay on the company plan, which would then coordinate benefits with Medicare as the secondary payer.

- “…or, if William prefers, offer a plan that is offered to the public”: This reflects the other choice available. Instead of keeping William on the group plan, the employer could offer to help him with a plan designed to work with Medicare, such as a Medicare Supplement (Medigap) plan or a Medicare Advantage plan. These are considered plans “offered to the public” on the individual market.

Option (b) is incorrect because it describes the rule for large employers (20 or more employees), which must offer the same coverage to all employees regardless of Medicare eligibility. Options (a) and (c) describe very specific types of plans (PACE and MSA) and do not represent the general options available to the employer. Option (d) correctly captures the flexibility that a small employer has in this situation.